Every Quote Is Free & Confidential

Every Quote Is Free & Confidential  What is the maximum loan termHere At First Choice Finance We Work With You |

|

The larger the amounts you need, the longer the term you are likely to have to plumb for. But even though you might want to keep your repayments tiny and take the interest on the chin the maximum loan term available to you is actually often down to the type of loan you take out, the lenders own criteria and also your age.

- Personal unsecured loans range from about £500 to £10,000, whilst usually offering terms ranging from 2 to 5 years, although a few personal loan providers do offer 7 years on some loan amounts. Terms are often quoted in months too, so at a stretch if you can borrow enough for your project via a personal unsecured loan you could spread the payments over 84 months.

To illustrate the payments through an example, a £10000 loan over 84 months at 12.9% APR would require monthly payments of £187.84 and a total paid back of £15778.56

To illustrate the payments through an example, a £10000 loan over 84 months at 12.9% APR would require monthly payments of £187.84 and a total paid back of £15778.56 - Secured loans are structured differently in that the lender has a charge over your property as added security much like with your mortgage. Because of this amongst other factors they can be used to borrow from £3,000 to £100,000 and allow a wider payment term, starting at 5 years and going up to 25 years. As an example of how this could be used for a £10,000 loan, if you took a 15 year (or 180 months) term the payments come down to £128.29 each, but the total payable would rise to £23092.20

- Mortgages are another well known and very established way to borrow larger sums, typically for house purchases or remortgaging your home to improve it etc. These also offer the lender security via a charge on your property giving more flexibility on amounts and terms. Lowest mortgage advances start at around £10,000 but can go up to millions of pounds. Terms here are the longest in the loan market with some mortgage providers tabling 35 year (420 months!) in certain scenarios. Opting for a 25 year term (300 months) on our £10,000 example gives monthly repayments of £112.94 with a total payback of £33882.

Now what we must bear in mind is we have used the same 12.9% rate in all 3 illustration and whilst the first two examples are likely to be fairly close in terms of rate mortgages tend to be lower, particularly at the moment with many being in the overall cost for comparison of between 4.9%APR.

We can see that amounts and terms are major ingredients when determining the longest term you can use from what is available in the market but the biggest impact on what you pay back is just as likely to be what interest rate you pay alongside the term and amount borrowed. For more information on long term loans available through our lending solutions or to try our online loan calculators .

|

|

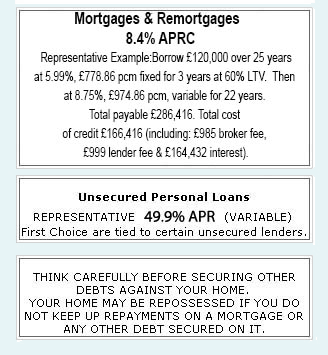

Unsecured Personal Loans |

THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST

YOUR HOME. |

Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk

Established In 1988. Company Registration Number 2316399. Authorised & Regulated By The Financial Conduct Authority (FCA). Firm Reference Number 302981. Mortgages & Homeowner Secured Loans Are Secured On Your Home. We Advice Upon & Arrange Mortgages & Loans. We Are Not A Lender.

First Choice Finance is a trading style of First Choice Funding Limited of 54, Wybersley Road, High Lane, Stockport, SK6 8HB. Copyright protected.